(Source: Ameriprise Financial Inc.)

Recently, Congress passed a new tax reform bill. Analysts at Ameriprise Financial have identified some areas that may affect taxpayers now and in the future.

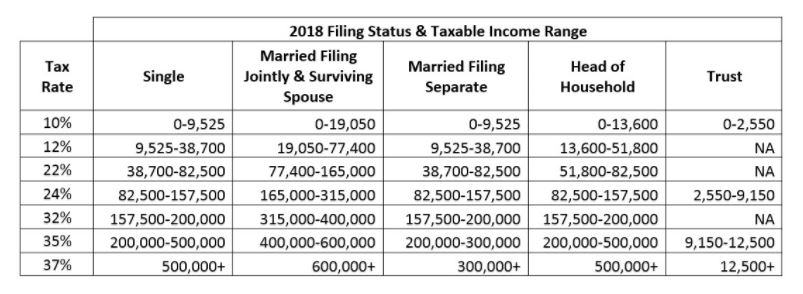

Tax rates and brackets

The law reduces tax rates and adjusts income brackets for taxpayers, including individual filers and married couples filing jointly. However, the number of individual tax brackets remains at seven. The number of estate and trust brackets is reduced from five to four brackets, also with slightly lower rates. These changes do not affect the special tax rates or tax brackets for long-term capital gains and qualified dividends.

The new tax rates and brackets apply from 2018 through 2025. (SEE CHART AT BOTTOM OF POST)

Standard deduction vs. more limited itemized deductions

The new law nearly doubles the standard income tax deduction for individuals to $12,000 (up from $6,350 in 2017), and to $24,000 (up from $12,700 in 2017) for married couples filing jointly. For taxpayers who have previously itemized their deductions, the increased standard deduction – as well as changes to itemized deductions – may make itemizing less attractive in 2018 for some.

Taxpayers should consider the impact of changes to itemized deductions made in the new law. These changes are in effect from 2018 through 2025.

- State and local itemized tax deductions will be generally limited to $10,000 but will apply to state and local property tax, plus either state and local income tax or sales tax, beginning in 2018.

- Charitable donation deductions remain in place, increasing limits for cash contributions to public charities from 50% to 60% of adjusted gross income (AGI), with some other minor changes.

- Mortgage interest deductions largely remain under previous rules. However, for homes purchased in 2018 through 2025, the existing $1,000,000 limitation is reduced to $750,000. Additionally, deductions are no longer allowed for interest paid on home equity loans for 2018 through 2025.

- Medical expense deductions are retained and, in fact, expanded for 2017 and 2018 to allow deductions for expenses in excess of 7.5% of AGI (prior rule is in excess of 10% of AGI).

- Miscellaneous itemized deductions are not allowed for 2018 through 2025, including:

Unreimbursed employee business expenses (e.g., travel expenses, home office expenses)

Investment fees and expenses

Tax preparation fees

Personal exemptions and child tax credit

Under the new bill, personal exemptions are eliminated for 2018 through 2025. However, during the same time, the child tax credit will be increased to $2,000 per qualifying child with a $500 credit for qualifying dependents other than qualifying children.

Other changes

- Recharacterization of ROTH conversions: Under the new law, “recharacterizing” a Roth conversion that occurs in 2018 is no longer possible. Recharacterizing Roth conversions that occurred in 2017 may still be possible depending on how the new law is interpreted by regulators. Recharacterizing Roth contributions to traditional IRA contributions and vice versa would continue to be permitted.

- Education savings/deductions: The tax advantages of 529 plans expand to K-12 education, allowing for tax-free withdrawals of up to $10,000 from qualified education savings accounts for private school tuition.

- Estate, Gift, and GST taxes: The federal transfer taxes are retained, but with an approximately double exclusion amount applicable for 2018 through 2025.

- 20% Deduction for Certain Pass-through Business Income: The bill provides a tax deduction for individuals, trusts and estates who own certain businesses operating as pass-through entities (sole proprietorships, partnerships, S corporations, and most LLCs). Eligible taxpayers can deduct up to 20% of the taxpayer’s allocable share of qualified pass-through business income, subject to limitations. For many businesses providing professional services (including financial advisors, doctors, and lawyers), the deduction is only available if the owner’s taxable income falls under certain thresholds ($315,000 married filing jointly, $157,500 otherwise), and the benefit is phased out over those thresholds (capped at $415,000 married filing jointly, $207,500 otherwise).

Contact your tax advisor if you have questions about the new legislation, and how it could affect you, and see your financial advisor. Though your Ameriprise financial advisor cannot provide specific tax advice, they can support your tax advisor and help you understand the general impacts of the legislation, or refer you to a tax advisor if you don’t already work with one.

Subscribe

Sign Up for Our E-Newsletter!

Stay up-to-date on all of the topics you care about by subscribing to our quarterly newsletter emailed directly to your inbox!

SubscribeSubscribe

Sign Up for Our E-Newsletter!

Stay up-to-date on all of the topics you care about by subscribing to our quarterly newsletter emailed directly to your inbox!

Subscribe